Africa’s Top 10 Digital Banks, Ranked

Nigeria is winning the customer race. South Africa proved neobanks can turn a profit. Here is who leads the continent’s banking revolution, and why it matters.

March 2026 | Customer Data, Leadership & Strategic Analysis

Africa’s digital banking sector is the fastest-growing in the world. Growth is no longer the question. Profit is.

The numbers tell a nuanced story. OPay reached its first monthly profit in 2024. PalmPay confirmed profitability in mid-2025, with revenue more than doubling since 2023. GoTyme Bank crossed into profit in December 2023. Capitec and Discovery Bank have been profitable for years. The challengers still chasing that milestone, Kuda, Chipper Cash, and Carbon, are competing in a sector where the rules are changing fast.

In early 2026, the story splits along two lines: Nigeria is about scale, adding tens of millions of first-time digital users every year. South Africa is about proof. The ten platforms below are ranked by customer reach, the clearest measure of adoption in markets where financial inclusion remains the primary challenge.

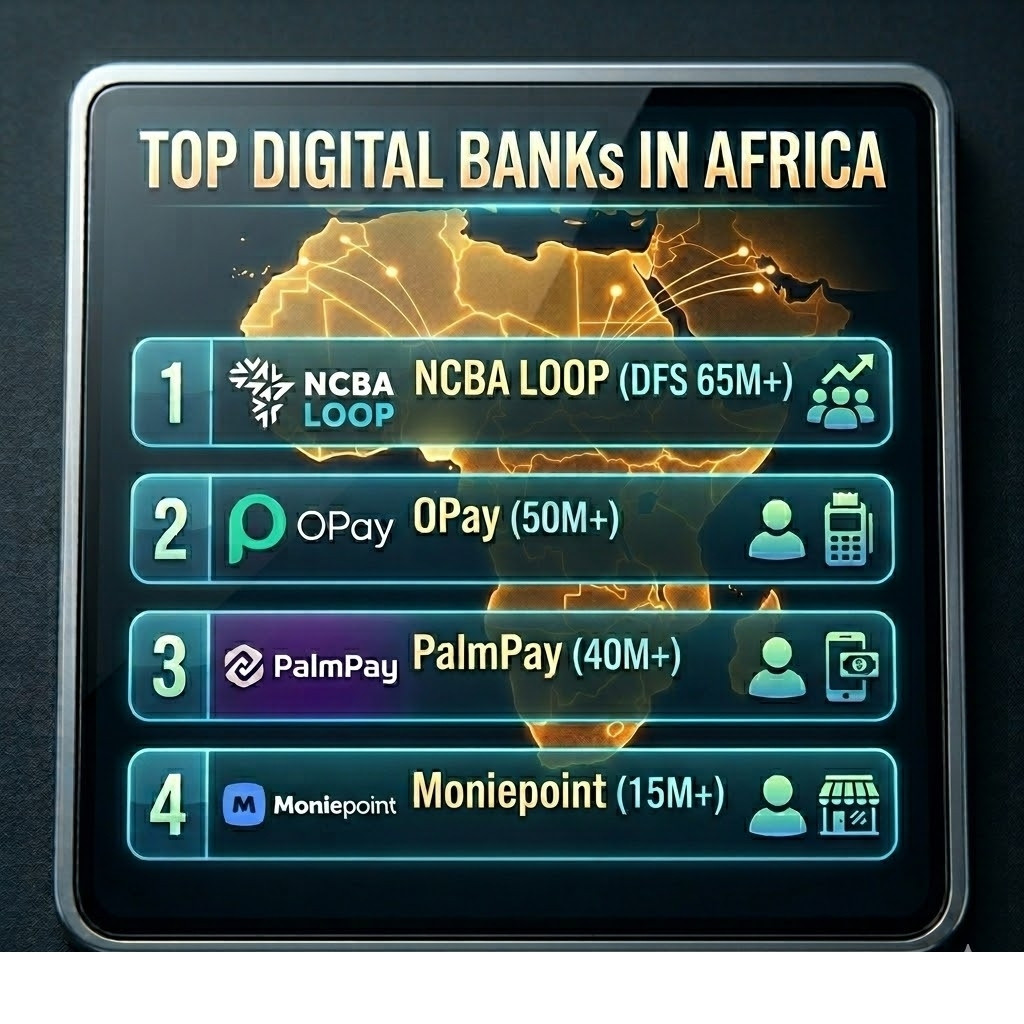

Africa’s Top 10 Digital Banks by Customer Reach

Estimated customer base, early 2026 (millions)

What the Numbers Actually Mean

1. NCBA LOOP DFS: The Platform Behind the Platform

The LOOP app looks like a lifestyle bank for Kenyan millennials. The real story is the infrastructure underneath. Eric Muriuki Njagi runs the fintech engine powering NCBA’s mobile-banking partnerships across six markets, including M-Shwari in Kenya, M-PAWA in Tanzania, and MoKASH in Uganda, Rwanda, and Côte d’Ivoire. By October 2025, LOOP DFS served over 60 million customers, a short-term credit and savings service embedded directly into M-Pesa, reaching people who would never enter a branch.

Nigeria did not digitize its existing banking customers. It created new ones from scratch.

2. OPay and PalmPay: Nigeria’s Agent-Network Bet

OPay (50M+) and PalmPay (40M+) together serve more customers than the entire South African top-10 combined. Neither did it through apps alone. Both built physical agent networks — touchpoints in markets, bus parks, and street corners — that convert cash into digital accounts. The first transaction is as simple as handing money to a neighbor with a phone.

3. GoTyme Bank (Formerly TymeBank): Profitable First

In December 2023, TymeBank became Africa’s first digital bank to post a profitable month, reaching that milestone in under five years from its 2019 launch. Under CEO Cheslyn Jacobs, who took the helm in January 2026, the rebrand to GoTyme Bank is complete. The global Tyme Group now serves 20 million customers across South Africa, the Philippines, Vietnam, and Indonesia. In SA alone, over 12 million customers bank with zero fees and five-minute digital onboarding.

4. Capitec and Discovery: The Traditional Banks That Got It Right

South Africa’s market is more mature. Customers are banked, demanding, and unforgiving of poor user experience. Capitec and Discovery Bank did not fight the digital wave. They built digital products that compete directly with fintech startups on experience, not just brand recognition.

Discovery Bank’s behavioral banking model, which rewards customers for healthy financial and lifestyle choices, has attracted 2.5 million users willing to share data in exchange for benefits. It is a fundamentally different value proposition to anything else on this list.

5. Moniepoint: Business Banking Done Right

While most Nigerian platforms chased consumer accounts, Tosin Eniolorunda built Moniepoint around small business owners. With 15 million+ customers and a product suite that covers business accounts, point-of-sale terminals, credit, and payroll, Moniepoint is the closest thing Nigeria has to a full-service digital business bank. In 2024, it became a unicorn. That is not a coincidence.

Customer Share by Country

% of top-10 total customer base

Nigeria’s Platforms vs SA

Combined reach, millions

The Platforms at a Glance

NCBA LOOP DFS

Kenya’s fintech infrastructure engine. Powers M-Shwari and cross-border mobile credit across 6 African markets. Expanding into embedded finance for trade, agriculture, and healthcare.

OPay

Nigeria’s largest mobile money platform. Agent-first model brings financial access to urban and semi-urban Nigerians. Backed by Chinese investors including Opera and SoftBank.

PalmPay

Transsion-backed digital wallet with deep agent network penetration. Focuses on Nigeria’s unbanked through reliable offline-to-online transaction rails.

Moniepoint

Nigeria’s business-banking platform of choice. POS terminals, credit, payroll, and accounts for SMEs. Unicorn-valued as of 2024. Expanding pan-Africa.

GoTyme Bank

Formerly TymeBank. Africa’s first profitable digital bank (Dec 2023). Rebranded Feb 2026. Zero monthly fees, 5-minute onboarding, part of global Tyme Group serving 20M customers worldwide.

Capitec Bank (Digital)

South Africa’s largest retail bank by customer count operates a full digital experience that rivals any fintech on UX. Profitable, growing, and still adding customers faster than its Big Four competitors.

Kuda Bank

Nigeria’s original pure-digital challenger bank. Zero-fee model and an app-first experience built the brand. Expanding to the UK and targeting the Nigerian diaspora.

Chipper Cash

Pan-African cross-border payments leader. Operates across Nigeria, Ghana, Uganda, Kenya, Rwanda, Tanzania, and South Africa. Focused on low-cost remittances and cryptocurrency rails.

Discovery Bank

Behavioral banking built on Discovery’s Vitality model. Customers earn rewards for financially responsible behavior. Premium positioning in South Africa’s most sophisticated banking market.

Carbon

Nigeria’s digital credit pioneer. One of the earliest African fintechs to offer instant mobile loans. Expanded to full banking with savings, payments, and business accounts.

Common Challenges Facing Digital Banks in Africa

Now that you know the players, you need to understand what they are all fighting against. Every platform on this list — regardless of size — faces the same six structural headwinds. These are not edge cases. They are the operating environment.

Regulatory Fragmentation

Africa has 54 countries and 54 different rulebooks. Licensing requirements, minimum capital thresholds, data residency rules, and consumer protection standards rarely align across borders. A platform that is fully compliant in Nigeria may need an entirely separate legal entity, product architecture, and compliance team to operate in Kenya or Ghana. For platforms targeting pan-African reach, regulatory arbitrage is not a strategy. It is a constant tax on expansion speed and capital.

High Cost of Customer Acquisition

Acquiring a digital banking customer in Nigeria or South Africa costs more than most platforms publicly admit. Agent commissions, referral bonuses, cashback incentives, and paid digital advertising stack up fast. Worse, switching costs are low. A customer who signed up for a free account and a N500 bonus has no structural reason to stay once the next platform offers N1,000. The platforms winning on acquisition cost are doing it through payroll partnerships, merchant networks, and retail kiosks — channels that bring sticky, active customers rather than incentivised sign-ups.

Infrastructure Reliability

A banking app is only as reliable as the network it runs on. Power outages disrupt agent terminals. Unstable mobile internet breaks onboarding flows mid-session. Interbank settlement systems go down during peak periods, turning routine transfers into hours-long disputes. In markets where a failed transaction is not just an inconvenience but can mean a missed rent payment or a business that cannot pay its suppliers, uptime is not a product feature. It is trust. Platforms that invest in offline-capable flows and local infrastructure redundancy build a real competitive advantage here.

KYC and Identity Gaps

Know-Your-Customer compliance is non-negotiable under banking regulations, but identity infrastructure across much of Africa remains thin. National ID coverage is incomplete. Document quality is inconsistent. Address verification is unreliable in informal settlements. Biometric databases are fragmented across agencies. The result is onboarding abandonment, manual review backlogs, and meaningful fraud exposure from synthetic identities. Platforms that have built proprietary identity verification — using telco data, facial recognition, or device fingerprinting — have a structural edge in both compliance speed and fraud prevention.

Fraud and Social Engineering

SIM swaps, phishing attacks, account takeover, and mule networks scale at the same speed as user growth. Fraudsters specifically target newly onboarded customers who are unfamiliar with digital banking norms and less likely to recognise a manipulation attempt. The financial losses from a single coordinated fraud campaign can eliminate months of margin. Platforms operating agent networks face an additional risk: agents themselves can become vectors for fraud, processing fake transactions or manipulating customers into sharing credentials. Fraud is not a technology problem. It is an organisational discipline problem that compounds without constant investment.

Interoperability Limits

Banks, mobile wallets, payment switches, and telcos often cannot move money between each other cleanly or instantly. Settlement disputes between platforms drag on for days. Customers who try to transfer from a neobank to a traditional bank account face delays, failed transactions, and opaque error messages. Cross-border transfers are worse — multiple correspondent relationships, currency conversion layers, and compliance checks turn a 10-minute transaction into a 3-day process. Until interoperability improves at the infrastructure level, every platform must either build bilateral integrations with every major counterparty or accept the limitations that come with a closed ecosystem.

10 Factors That Separate Profit from Scale

Customer numbers get you funded. These ten disciplines get you to profit. Every platform that has crossed into the black has mastered most of them. Every platform still burning cash has not.

Pricing Discipline

You charge for value, not for volume. Free-forever products attract users but train them to churn the moment a competitor offers a better bonus. Profitable banks price their products to reflect the cost of serving each customer, then earn loyalty through reliability and experience rather than subsidies. The “bank of the free” model works only when lending margins cover the acquisition and servicing cost of the free accounts. If they do not, you are running a marketing company with a banking licence.

Low-Cost Acquisition

The profitable platforms win customers through payroll partnerships, merchant networks, retail kiosks, and agent channels — not paid ads and cashback campaigns. GoTyme Bank places kiosks inside Pick n Pay and Boxer stores. Moniepoint acquires SME clients through its POS terminal network. Capitec captures customers at point-of-salary. Each of these channels delivers an active customer at a fraction of the cost of digital advertising, and with a far higher lifetime value.

High Activity Per Customer

A dormant account costs money and generates none. Daily-use behaviours — airtime top-ups, merchant payments, utility bills, peer transfers — are the engine of unit economics. Platforms that embed banking into daily spending habits rather than treating it as a monthly login event generate five to ten times the revenue per customer from the same base. Engagement frequency is the metric that separates a profitable cohort from a costly one.

Strong Deposit Engine

Sticky deposits are cheap funding. Salary accounts, merchant settlement balances, and savings products keep customer money on platform long enough to fund lending at a cost that makes the interest margin work. Banks that rely on expensive wholesale funding or that cannot retain deposits between payday and the next bill payment are structurally disadvantaged. Capitec built its lending business on a foundation of low-cost retail deposits captured through payroll — the same playbook GoTyme Bank is now executing at scale.

Smart Credit Strategy

The fastest way to destroy a digital bank is to lend aggressively before collections infrastructure is proven. Profitable lenders start with small ticket sizes and short loan tenors, use mobile transaction history and repayment behaviour to refine scoring, and expand credit limits only when default rates stay within model. Moniepoint scores SME borrowers using live POS transaction data rather than self-reported income. Carbon built its credit engine over years before scaling loan volumes. The discipline to grow slowly in credit is the single largest determinant of survival.

Risk and Fraud Control

SIM swaps, account takeover, and mule networks scale at the same speed as user growth. A single coordinated fraud campaign can eliminate months of margin. Profitable platforms automate fraud scoring in real time, flag anomalous transaction patterns before settlement, and build friction into high-risk flows without degrading the experience for legitimate users. Fraud is not a technology problem — it is an organisational discipline that requires constant reinvestment as attack vectors shift.

Efficient Operations & Automation

KYC verification, dispute resolution, reconciliation, and customer support are the four largest operational cost centres in retail banking. Platforms that automate all four reduce cost-per-account as volume rises rather than adding headcount proportionally. A bank serving one million customers at $5 each per year in operational cost that drops to $1.50 at ten million users has built a structurally profitable business. One that adds a support agent for every 2,000 new customers has not.

Payments Reliability & Uptime

Failed transactions are not just a customer experience problem — they are a direct cost. Each failure generates a support ticket, a potential chargeback, and a reason for a customer to open an account elsewhere. Platforms with consistently high uptime and low dispute rates spend less on resolution and retain more customers. In markets where power instability and variable connectivity are structural realities, offline-capable flows and local infrastructure redundancy are a genuine competitive advantage.

Balanced Product Mix

Payments are high-volume but low-margin. Credit, merchant services, insurance, and FX earn real margin. One-product banks struggle because a single revenue line leaves no buffer when volumes dip or regulators intervene. Discovery Bank earns on lending, insurance, and Vitality rewards data simultaneously. Moniepoint stacks POS hardware fees, merchant transaction fees, and working capital loans on the same SME relationship. The more margin layers built on a single customer, the more resilient the business model.

Regulatory & Settlement Discipline

Liquidity management, prefunding requirements, and settlement timing are not compliance footnotes — they are cash flow. A platform that mismanages settlement cycles faces funding gaps that force expensive short-term borrowing. A compliance failure in one market can freeze the entire group’s expansion plans while regulators review. The banks that treat regulatory relationships as a strategic asset rather than an obstacle tend to get faster licence approvals, more constructive supervisory dialogue, and fewer operational surprises.

What Comes Next

The race in 2026 is not just for customers. Any platform with enough agent-network capital can acquire a million users. The real competition is for sustainable revenue, cross-border scale, and the trust of users who have been burned before.

Nigeria’s giants will face pressure from regulators who are tightening oversight of agent networks and mobile money services. South Africa’s GoTyme Bank and Capitec will push into each other’s territory as both target the mass-market customer. And the pan-African platforms, Chipper Cash chief among them, are betting that the continent’s 54 countries become one connected payments market sooner rather than later.

Every platform on this list is making a different bet on what Africa’s financial system looks like in 2030. Scale got them here. Profitability, trust, and cross-border reach will separate the survivors from the rest.