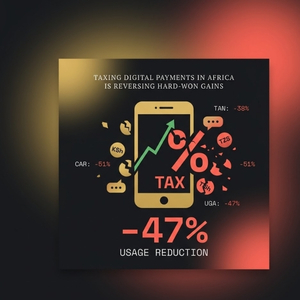

Taxing Digital Payments

in Africa Is Reversing

Hard-Won Gains

Africa built one of the world’s most advanced mobile payment ecosystems. Governments are now taxing it into retreat. The data across Uganda, Tanzania, Cameroon, and now Kenya tells one consistent story.

Africa built one of the world’s most advanced mobile payment ecosystems over two decades. Governments are now taxing it into retreat.

By Q3 2025, about 20 sub-Saharan African countries had introduced some form of mobile money tax. The justification is fiscal pressure. The result is the same in every market: fewer transactions, less digital adoption, and the unbanked going back to cash.

The Numbers Tell One Story

The data is not ambiguous. Across every market that has introduced a mobile money tax above the GSMA’s 0.2% threshold, the same pattern plays out. Transaction volumes fall. Users disengage. Revenue misses targets. Governments scramble to revise policy.

The GSMA identifies a clear tipping point: once a tax exceeds 0.2% of transaction value, users change behavior measurably — shifting back to cash. The IMF’s price elasticity is −2.1: a 10% cost increase produces a 21% drop in transaction volume. Most African countries with mobile money taxes sit well above this threshold.

Who Bears the Heaviest Load

These taxes are not neutral. IMF research confirms they are regressive. They increase transaction costs disproportionately on those with the lowest income. Small transactions — the type made by low-income households and micro-businesses — absorb the highest relative cost.

Rather than capturing new revenue, governments push users back to cash and eliminate the digital trail that improves credit access for the unbanked.

“The people these policies hit hardest are the ones digital finance was supposed to reach first.”

FinHive Africa Editorial · May 2026A Decade of Progress at Risk

The share of adults in Sub-Saharan Africa with a bank or mobile money account grew from 34% to 58% between 2014 and 2024. By 2024, 51% of all African adults had made or received a digital payment. In 2023, mobile money contributed approximately $190 billion to SSA’s GDP.

That growth happened because digital payments were accessible and affordable. Tax them past the tipping point and the growth stalls — or reverses.

| Country | Tax Applied | Measured Impact | Policy Outcome |

|---|---|---|---|

| Uganda | 1% → reduced to 0.5% | −24% transactions | Partially reversed |

| Tanzania | Up to 10% on withdrawals | −38% in 3 months | Policy revised |

| Cameroon | % on transaction value | −40% avg. monthly value | Still active |

| Central African Rep. | 1% on P2P & withdrawals | −51% per user | Still active |

| Zambia | Tax doubled Jan 2025 | Weaker corporate revenues | Under review |

| Ghana | Mobile money levy | Adoption slowdown | Tax removed ✓ |

| Chad | Mobile money tax | Usage declined | Plans to remove ✓ |

Governments Are Learning, Slowly. And Some Are Not.

Some countries are correcting course. Chad plans to remove its tax. Ghana already has. Gabon rejected a similar proposal in parliament. These reversals confirm what the data showed from the start: taxing digital transactions at the user level shrinks the ecosystem and reduces the fiscal yield governments were chasing.

Kenya is moving in the opposite direction. The country often cited as the continental benchmark for digital payment adoption is now proposing one of the most sweeping expansions of digital payment taxes in Africa.

Kenya’s Finance Bill 2026 proposes a 16% VAT on all 42 licensed payment service providers — including M-Pesa, Pesapal, Airtel Money, and Kenswitch. Treasury says the tax targets platform owners, not users. The distinction is unlikely to hold.

Tax experts, including PKF Kenya’s Michael Mburugu, say PSPs will pass the cost to consumers through higher transfer fees. The Bill also proposes a 25% excise duty on smartphones — taxing both the device needed to access digital finance and the platform used to transact on it.

The structural bias embedded in the Bill tells the full story.

This is a policy contradiction Kenya cannot afford. The country built a digital payment lead the rest of Africa studied and replicated. That lead was built on affordable access. The Finance Bill 2026, if passed as proposed, erodes the cost advantage that made M-Pesa the default financial tool for 37 million low-income Kenyans.

Kenya has Uganda, Tanzania, and Cameroon data to draw from. Choosing to replicate their mistakes is a policy choice, not an oversight.

There Are Better Options

The argument is not that digital platforms should never contribute to the fiscal base. The argument is that taxing citizen transactions at the point of use is the wrong mechanism. Alternatives exist and some African governments are already applying them.

Finance ministries are treating digital payments as a revenue extraction point rather than infrastructure. For millions of Africans, mobile money is not a luxury product. It is the only financial system they have access to. Tax it into retreat and you lose the users, the data trail, the merchant activity, and the decade of financial inclusion progress it took to build.